Micro or Non-Micro Company?

Under certain conditions a micro-enterprise pays more in taxes than a regular LLC. It is easy to notice that a micro-enterprise is advantageous if a balance has been found between the number of employees and revenue.

Let us imagine a situation: there are two companies, each with 5 employees, each of whom receives 720 EUR net per month. For simplicity of calculation, let us assume that value added tax (VAT) is not calculated and there are no expenses.

Regular LLC:

To pay out a net salary of 720 EUR, 43.57% must be paid in taxes from the imagined amount X, and moreover the non-taxable minimum and dependant allowances are in force. This is significant, because the micro-enterprise does not have this. As a result, to pay out a net salary of 720 EUR, 555.86 EUR will be paid in taxes, and the entrepreneur will need to reserve (amount X) - 1,275.86 EUR.

Micro-enterprise (LLC, micro-enterprise status only):

9% of all (!) revenue is paid in taxes. This is the only tax. Restriction - the salary may not exceed 720 EUR/month, and the company's turnover may not exceed 100,000 EUR/year. It may, but then the company loses its micro-enterprise status.

Some clarifications: Salary is the amount comprising the employee's net wages plus taxes. Since the planned net pay-out is 720 EUR, in the case of a regular company one would need to earn 1,275 EUR (720 + 555)/month, while in the case of a micro-enterprise - 784 EUR (720 + 64)/month.

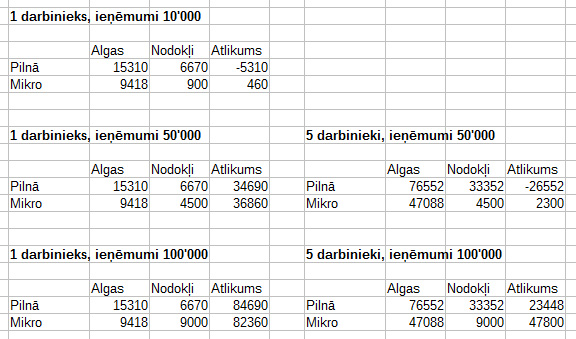

Figure 1.

In Figure 1 we can see that under certain conditions a micro-enterprise pays more in taxes than a regular LLC. It is easy to notice that a micro-enterprise is advantageous if a balance has been found between the number of employees and revenue (for example, 1 employee and up to 70,000 EUR in revenue, 2 employees and up to 140,000 EUR). Meanwhile, for a regular LLC tax payments are constant and dependent on the number of employees, so with high revenue but an unchanged number of employees, the company's owners have a greater opportunity to obtain larger dividends.

One might argue that there is a discernible lobby of large companies (perhaps even with foreign capital), but tying taxes to revenue in no way promotes the desire to reinvest profits in equipment. Increasing the MUN (micro-enterprise tax) from 9% to 11% will further reduce this desire.

comments